From 1 January 2025, the special VAT regime (the SME scheme) allows small enterprises to:

- sell goods and services without charging VAT to their customers (VAT exemption) and,

- alleviate their VAT compliance obligations.

Small enterprises choosing VAT exemption will lose the right to deduct VAT on goods and services used to make exempt supplies.

Have a look at the campaign material page for more information.

Who can benefit?

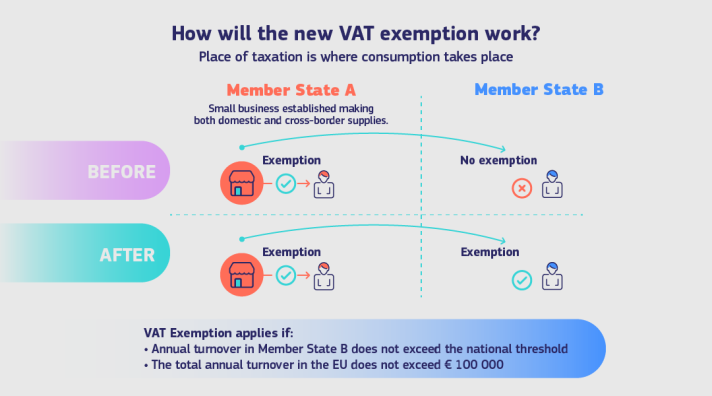

Any small enterprise with a total annual turnover of no more than EUR 100 000 (or the equivalent in national currency) in all Member States in the current calendar year and in the previous calendar year is eligible for the VAT exemption in its Member State of establishment (MSEST) and/or in other Member State(s) under the cross-border SME scheme.

This is applicable only if the Member State concerned has implemented the scheme in its national legislation.

The SME scheme is optional.

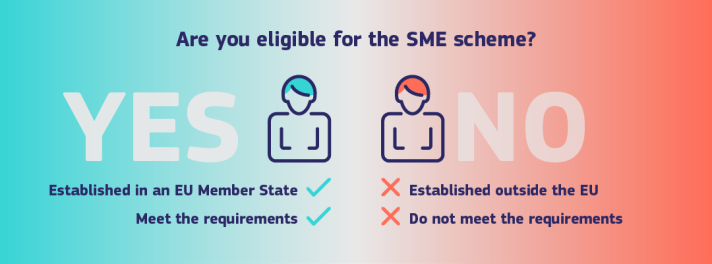

Non-EU small enterprises cannot apply the SME scheme. In the context of the SME scheme, small enterprises established in the United Kingdom, including Northern Ireland, are non-EU small enterprises.

What’s new?

New maximum for national annual threshold

The maximum national annual threshold set by Member States under which small enterprises can VAT exempt their supplies of goods and services under the SME scheme (domestic and cross-border) is EUR 85 000 (or the equivalent in national currency).

Member States have the possibility to set more than one national annual threshold. These are called ‘sectoral thresholds’. In case a small enterprise can benefit from more than one sectoral threshold, the tax authorities will, based on its activities, inform the small enterprise about the threshold to use since only one threshold can be applied per taxable person.

Cross-Border Application

Small enterprises established in another Member State than where VAT is due can VAT exempt their supplies (cross-border), in the same way that small enterprises established in that Member State already can for domestic transactions.

This will help place all small enterprises on an equal footing, whether they are based in that Member State or not.

Union annual threshold

Small enterprises with a total annual turnover in the 27 Member States not exceeding EUR 100 000 are eligible to apply the cross-border SME scheme.

You can check your eligibility on the simulator.

Simplified compliance

- Single registration: small enterprises will only need to register for the purpose of the SME scheme once in the MSEST. MSEST will grant a single identification ‘EX number’ that will be used in all Member States where the small enterprise benefits from the VAT exemption.

- Single quarterly report: periodical VAT returns are replaced by one single quarterly report to inform about the turnover of the small enterprise in all Member States.

- Simplified invoices

Which goods and services are eligible for VAT exemption?

All supplies of goods and services are eligible, with some exceptions.

What are the conditions for applying the SME scheme?

The conditions depend on whether you apply the domestic SME scheme only or the cross-border SME scheme.

Rules applicable as of 1 January 2025

You already apply the domestic SME scheme in your Member State of establishment and may want to continue so. In this case, domestic rules will apply.

| Situation on 31 December 2024 | Situation on 1 January 2025 | Rules to apply |

|---|---|---|

| I apply the domestic SME scheme | I want to continue applying the domestic SME scheme | Domestic rules |

It may be that you already apply the domestic SME scheme in your Member State of establishment but do not want to apply it anymore or you may not yet apply the SME scheme but want to start applying it there. Also in these cases, domestic rules will apply. On procedures to follow when leaving or accessing the domestic SME scheme, you should turn to your Member State of establishment.

| Situation on 31 December 2024 | Situation on 1 January 2025 | Rules to apply |

|---|---|---|

| I apply the domestic SME scheme | I don’t want to apply the SME scheme anymore | Consult your Member State of establishment to learn about the procedure (if any) to leave the domestic SME scheme. |

| I do not apply the SME scheme | I want to start applying the SME scheme in my Member State of establishment only (domestic). | Contact your Member State of establishment to learn about the procedure (if any) to access the domestic SME scheme. |

You already apply the domestic SME scheme in your Member State of establishment and may want to continue (or stop) applying it there but also want to start applying the SME scheme in other Member States (cross-border SME scheme). Or if not already applied in your Member State of establishment, you want to start to apply the SME scheme in other Member States whether or not you want to start applying it also in your Member State of establishment. In all these cases, cross-border rules will apply.

| Situation on 31 December 2024 | Situation on 1 January 2025 | Rules to apply |

|---|---|---|

| I apply the domestic SME scheme | I want to apply the SME scheme in my Member State of establishment and in other Member State(s) (cross-border). | Cross‑border rules |

| I apply the domestic SME scheme | I want to stop applying the SME scheme in my Member State of establishment but want to apply the SME scheme in other Member State(s) (cross-border). | Cross‑border rules |

| I do not apply the SME scheme | I want to apply the SME scheme either in my Member State of establishment and in other Member State(s) or only in Member State(s) other than my Member State of establishment (cross-border). | Cross‑border rules |

FAQ

What is a small enterprise?

In the context of the SME scheme, a small enterprise refers to any person considered to be a taxable person for VAT purposes, regardless of their form (self-employed, freelancer, start-up, incorporated company, natural person carrying out economic activity, etc.) and whose annual turnover within the European Union does not exceed EUR 100 000 (cross-border SME scheme).

Which Member State is the Member State of establishment?

The Member State of establishment (MSEST) is the Member State where the business’ central administration carries out its functions. For a natural person (freelancer, entrepreneur, etc), the Member State of establishment can be where it has its permanent address. To ensure effective application of the scheme, there can be only one Member State of establishment.

For the application of the SME scheme, the place of establishment does not cover fixed establishment as that could lead to multiple identifications under the SME scheme. This means that a Member State where a small enterprise has a fixed establishment cannot be the MSEST.

Can a small enterprise established outside the EU with a fixed establishment within the EU apply the SME scheme?

No. Only small enterprises established in an EU Member State can have access to the SME scheme.

Can a small enterprise apply the SME scheme in an EU Member State that has not implemented the SME scheme?

No. It is not possible to apply the SME scheme in a Member State that has not implemented it.

Can a small enterprise established in a Member State that has not implemented the SME scheme apply the cross-border SME scheme in other Member States?

Yes. Small enterprises established in a Member State (Member State of establishment) that has not implemented the SME scheme can still have the possibility to access the cross-border SME scheme in other Member States. Small enterprises will submit the prior notification and the quarterly reports in their MSEST which will act as the contact point with the other Member States (Member States of exemption).

Is the SME scheme suitable for my business?

The SME scheme is optional. Small enterprises should assess whether this scheme is suitable to their specific situation or if it is preferable to stay under the standard VAT regime. The SME scheme can be suitable, for instance, if the small enterprise is involved in distance sales to final consumers.

Can a start-up apply the SME scheme if its annual turnover is zero?

Yes. A start-up and any small enterprise starting an economic activity can apply the SME scheme – domestic or cross-border – if it fulfils the requirements. In that case, the annual turnover to report in the prior notification and in the quarterly report would be zero ‘0’.

Which goods and services are eligible for VAT exemption under the SME scheme?

All supplies of goods and services are eligible, except:

- Occasional transactions, such as the supply before the first occupation of a building or parts of the building or the supply of building land,

- Exempt cross-border supplies of new means of transport made from one Member State to another.

- Additional transactions excluded by the Member State concerned.

The Member State where I want to apply the VAT exemption has sectoral thresholds. Which threshold shall I use?

For the domestic SME scheme: you should contact your Member State of establishment.

For the cross-border SME scheme: in the prior notification, the annual turnover must be broken down per threshold. On that basis the tax authorities of the Member State granting the exemption will inform the small enterprise – through the Member State of establishment – which sectoral threshold applies.

Example A Member State has two sectoral thresholds: one for the construction sector and one for all other economic activities. In case a small enterprise could benefit from both thresholds, the tax authorities of that Member State will inform the small enterprise which threshold it should use for the current calendar year. At the end of each year, tax authorities can reassess the threshold to be used for the upcoming year. |